The AI Hardware Revolution

1. The Great Leveling: The Shift to Open-Source

For the last several years, the AI sector has functioned like a professional marathon where only the most well-capitalized tech incumbents could compete.

These entities owned the track, controlled the coaching staff, and hoarded the training regimens for all the right reasons to raise money and pioneer the market.

However, the arrival of China’s Zhipu’s GLM 5.2—a highly capable open-source model—has challenged the playing field.

The arrival of GLM 5.2 is a critical catalyst for the industry for three primary reasons:

Frontier-Level Benchmarking: It closes the performance gap with closed-source American models, particularly in “agentic work,” the most valuable frontier of AI capability.

Democratized Infrastructure: As an open-source asset, it is free to download, fine-tune, and deploy on private servers, removing the “toll” previously required to access high-end intelligence.

Hyper-Accelerated Adoption: Developer activity on platforms like Open Router is currently outstripping the massive adoption spikes seen with DeepSeek in April, signaling a rapid migration toward open-source foundations.

This shift transforms the underlying unit economics of AI: the “brain” is no longer a high-variable API expense (OPEX), but a portable asset that can be run on local hardware, shifting the focus from software licensing to physical silicon logistics.

2. Understanding Agentic AI: The “Brain” Behind the Hardware

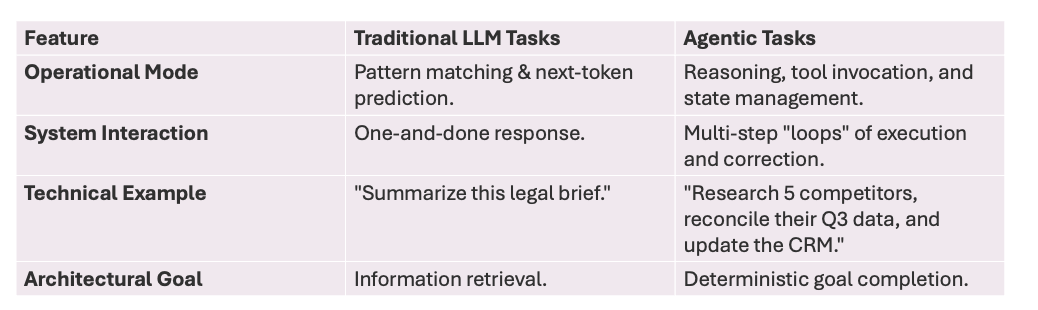

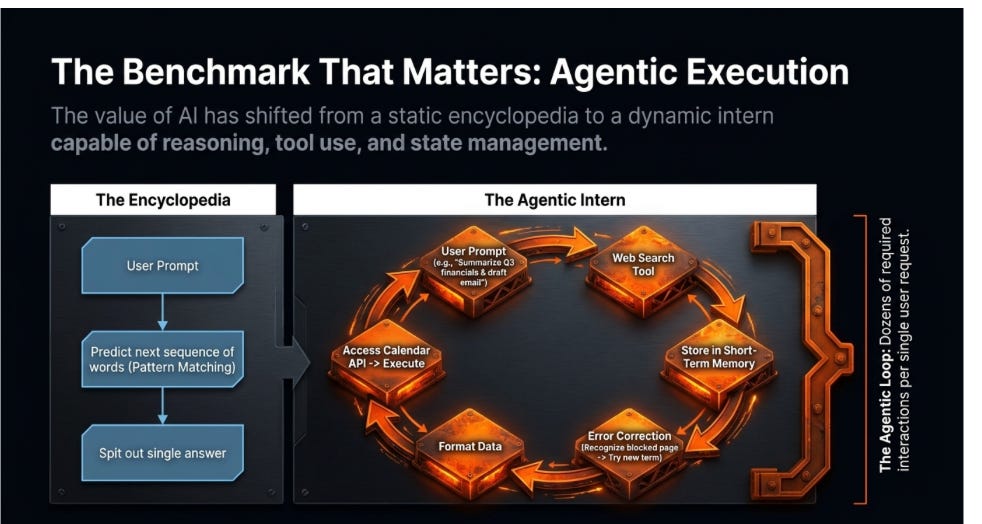

To architect effective AI systems, we must distinguish between standard pattern matching and Agentic AI.

While traditional models serve as a “Smart Encyclopedia” for querying facts, agentic models act as a “ Mixture of Experts” capable of autonomous execution.

Features, Traditional LLM Tasks, and Agentic Tasks

The “Loop” Problem: Agentic work is not just about saying things; it is about doing things.

This requires the model to open browsers, recognize blocked pages, correct errors, and manage state across dozens of back-and-forth interactions.

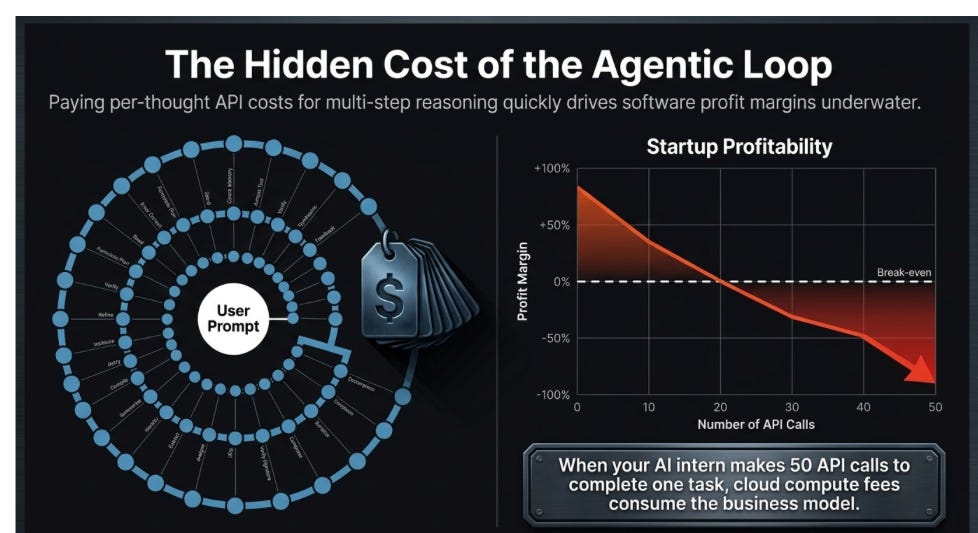

In a closed-source ecosystem, every “thought” in this loop incurs a variable API overhead.

If an agent requires 50 calls to complete one task, a startup’s profit margins are quickly consumed by cloud compute fees using the Mixture of Experts in the LLM and “jacking” token IN/OUT costs.

Open-source models attempt to eliminate this financial bottleneck, thereby reducing the marginal cost of complex reasoning.

This economic reality is driving a massive enterprise pivot toward local execution and data sovereignty.

Note: Adjusting for Spin. Initial testing and adoption are strong, according to Open Router and Hugging Face. But your mileage will vary depending upon your own testing and access to internal AI teams or partners.

3. The Enterprise Pivot: Privacy and the “Medical Residency” Analogy

Major players are moving toward open-source models to prioritize Data Portability and security.

In high-stakes industries, sending sensitive data to an external third-party model—even with encryption—is a vulnerability.

It is the equivalent of handing a locked briefcase to a courier.

By utilizing open-source models, enterprises can keep their data “Airgapped,” running models entirely behind corporate firewalls to eliminate external exposure.

The “Medical Residency” Analogy: Enterprises utilize fine-tuning to transform generalized base models into specialized experts:

The Base Model: Like a brilliant medical graduate with a generalized understanding of biology (the billions-of-dollars training phase).

Fine-Tuning: Like a six-month residency where the graduate learns a specific hospital’s rare cardiac imaging and filing systems.

Architecturally, fine-tuning is highly efficient; it costs thousands of dollars rather than billions. Crucially, it reduces the need for the massive networking bandwidth required by global clusters, allowing specialized expertise to live on localized hardware.

To further optimize costs, leaders are using Model Routing: directing simple queries to low-cost, local open-source models while reserving premium closed models for high-complexity reasoning.

As models move in-house, the industry’s primary challenge shifts from software access to the efficiency of the underlying silicon.

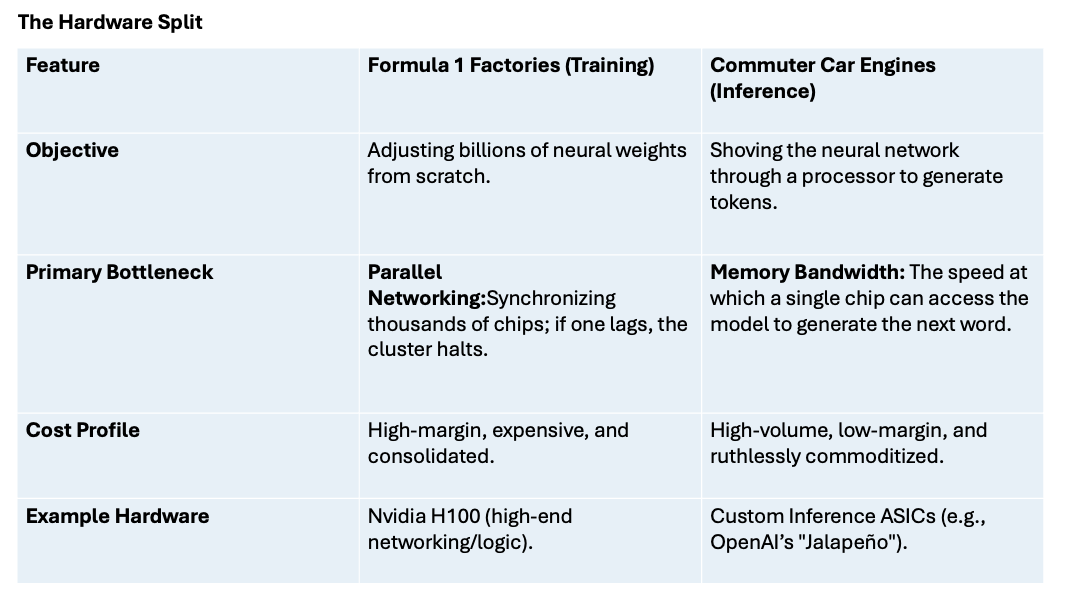

4. The Hardware Great Divide: Training vs. Inference

The hardware market is splitting into two distinct sectors: the massive clusters required to build models and the efficient engines required to run them.

The world has moved past the era where “factories” were the only priority. With frontier models now available for free, the race is on to design the “commuter engines” that can run these models locally with maximum efficiency.

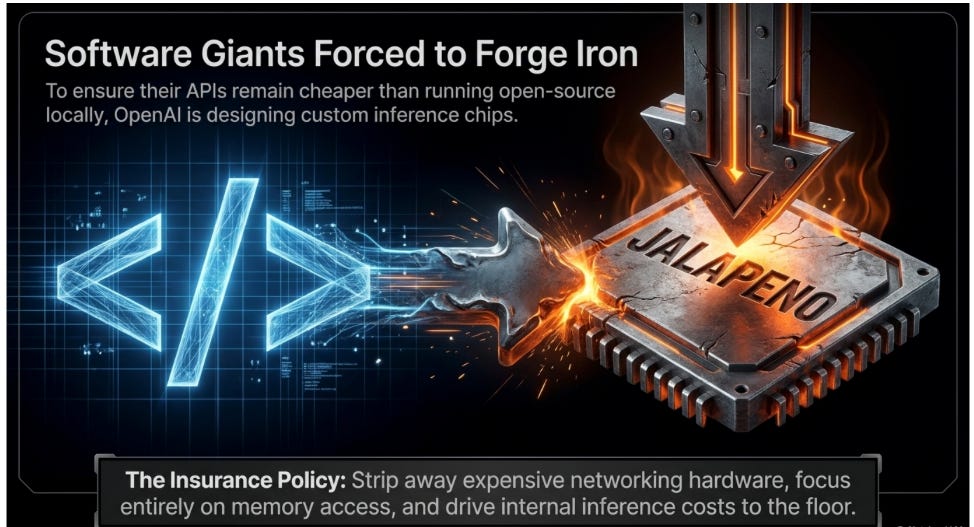

5. Silicon Logistics: The Rise of Custom Chips

Because inference costs are the new bottleneck, software companies are moving down the stack. OpenAI’s rumored custom chip, “Jalapeño,” serves as an “insurance policy.” If OpenAI can drive its internal inference costs below the cost of running an open-source model, it maintains its competitive moat.

The Evolving Competitive Landscape:

NVIDIA: Currently dominant in training, NVIDIA faces a “war on two fronts.” It must defend its high-margin training business while competing in a low-margin, commoditized inference market where specialized ASICs are often more efficient than general-purpose GPUs.

Broadcom: A primary beneficiary of this fragmentation, providing the custom networking and manufacturing logistics for companies like Google and Meta as they build their own internal silicon.

OpenAI/Google/Meta: These giants are pursuing internal custom silicon to drive the marginal cost of AI toward zero, ensuring they aren’t held hostage by external hardware pricing.

This structural shift aims to make running AI daily so cheap that it becomes as ubiquitous as electricity.

6. Conclusion: Where the Value Lives in 5 Years

The AI landscape is being fundamentally rewired. As foundational models become commodities and the silicon to run them enters a race to the bottom, the traditional competitive moats are evaporating.

In the next five years, the ultimate “winners” will not be those who own the biggest models or the fastest chips. Instead, value will reside in:

Proprietary Data: The unique, high-quality information used for specialized fine-tuning.

Strategic Vision: The ability to architect systems that know which questions to ask and which problems are worth solving.

Local execution and data portability are the new requirements for success.

The next era of AI will not be won by the company with the most expensive gear, but by those with the vision to use open-source models and invest in people to build out the AI Enterprise Stack.